Distressed properties have become one of the hottest opportunities in real estate investing. Whether you’re a seasoned investor or just getting started, buying a distressed asset can open the door to substantial profit margins—if you know what you’re doing. But with opportunity comes risk, and understanding those risks is essential.

This guide breaks down what a distressed property is, how to evaluate one, financing options, and what every investor should know before diving in.

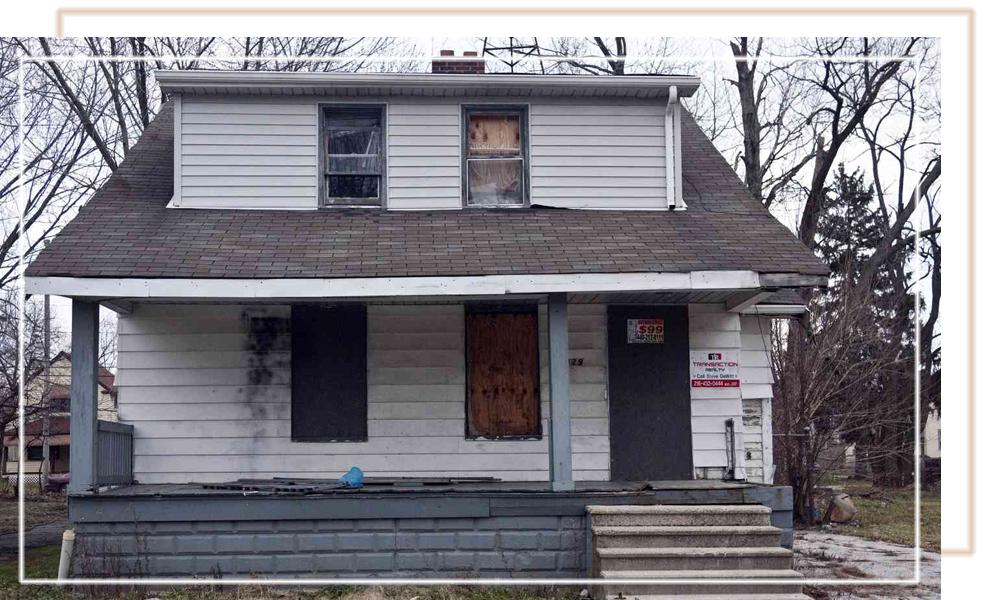

What Is a Distressed Property?

A distressed property is real estate that is under some form of financial or physical distress. This usually means:

The owner has fallen behind on mortgage payments.

The property is in pre-foreclosure or foreclosure.

The asset is physically neglected or in poor condition.

There may be tax liens, code violations, or other legal issues attached to the property.

Distressed properties are often sold at a discount—making them attractive for fix-and-flip investors, BRRRR investors, and buy-and-hold landlords.

Types of Distressed Properties

Understanding the type of distress helps you determine the right strategy and the level of complexity involved.

1. Pre-Foreclosure

The homeowner has missed several mortgage payments but the home hasn’t yet been auctioned. These deals often offer:

Motivated sellers

Below-market prices

Opportunities for negotiation

2. Foreclosure / Auction Properties

The lender has taken legal action and is selling the home at auction. Benefits include pricing, but risks include:

Limited inspections

Cash-only requirements

No guarantees

3. REO (Real Estate Owned) Properties

These are properties the bank couldn’t sell at auction. Pros:

Clear title

Potential for financing

Negotiable pricing

4. Physically Distressed Homes

These need significant repairs due to:

-

Neglect

-

Fire or water damage

-

Structural issues

-

Code violations

These can deliver strong returns—but only if you know rehab costs accurately.

Why Investors Seek Distressed Properties

Investors focus on distressed properties for several reasons:

✔ Below-Market Pricing

Because distressed assets come with problems, sellers (or lenders) typically accept discounted offers.

✔ High ROI Potential

After rehab, the property can be resold or rented for significantly more than the purchase price.

✔ Less Competition in Certain Markets

Many retail buyers will not touch distressed inventory due to financing limitations or repair concerns.

✔ Ideal for BRRRR Strategy

Distressed properties are perfect candidates for:

Buy → Rehab → Rent → Refinance → Repeat

Risks You Need to Consider

While the upside can be big, distressed property investing is not for beginners who move blindly.

1. Unexpected Repair Costs

Properties often have hidden structural, mechanical, or safety issues.

2. Title Problems

Liens, unpaid taxes, and other obligations can turn a great deal into a financial burden.

3. Limited Access for Inspections

Some auction or pre-foreclosure properties are sold as-is, with little or no walkthroughs.

4. Financing Limitations

Traditional lenders may not fund properties in poor condition, forcing buyers to rely on hard money loans, private capital, or cash.

5. Timeline & Holding Costs

Delays in rehab, permitting, or eviction (if needed) can erode profits.

Increase Profit on Fix and Flip Projects

Maximize your profits with smart fix-and-flip strategies. Learn how to choose the right property, control renovation costs, secure optimal financing, and boost resale value to achieve higher ROI on every investment.

How to Properly Evaluate a Distressed Property

Before making an offer, investors should take these steps:

✔ Run Accurate ARV (After Repair Value)

This is the projected value of the property once renovated. It determines:

Maximum offer price

Loan approval

Profit margin

A common formula many investors use is:

MAO (Maximum Allowable Offer) = (ARV × 0.70) − Repair Costs

✔ Order a Comprehensive Title Search

Never assume title is clean—verify it.

✔ Estimate Rehab Costs Carefully

Use licensed contractors when possible, and account for:

Labor shortages

Material increases

Surprises behind the walls

✔ Understand the Exit Strategy

Are you flipping, renting, refinancing, or holding long-term?

Your exit strategy determines your ideal loan type.

✔ Know the Market

Study:

Rental comps

Flip comps

Days on market

Homebuyer demand

A distressed home in a declining neighborhood is rarely a good investment.

Financing Distressed Properties

Traditional lenders usually won’t touch distressed real estate, especially if the home needs major repairs. That’s why most investors rely on:

✔ Hard Money Loans

Fast, asset-based loans ideal for:

Benefits:

Quick closings (3–7 days)

Flexible guidelines

Rehab funds included

✔ Private Lenders

Individual investors who fund deals for interest returns.

✔ Cash Purchases

Still the most competitive method—especially at auctions.

Tips for New Investors

If you’re just getting into distressed property investing, follow these best practices:

Start with a project that needs cosmetic work, not structural overhauls.

Build a contractor team you trust.

Work with a lending partner that understands distressed assets.

Always account for a buffer in your budget (10–20%).

Treat it like a business, not a hobby.

Final Thoughts

Distressed properties can be a powerful path to wealth—but only if you’re prepared. Understanding the risks, running your numbers accurately, and leveraging the right financing can make the difference between a profitable project and a costly mistake.

If you’re exploring distressed properties and need funding for your next fix-and-flip or BRRRR deal, partnering with a reliable hard money lender like JCREIG Capital Funding can help you move quickly and confidently.

How To Invest In Distressed Real Estate

YOU run the deal — we just fund it.

Unlock the potential of distressed properties. Learn how investors identify, fund, and profit from distressed real estate opportunities.

👉 Submit a deal for review.

or reach out to us @ 561-303-0334 if you require funding or have any questions.

{kind=link}